Corporate bonds are better positioned than Treasurys.

Given the current fiscal environment, expected path of the Federal Reserve (Fed), and geopolitics, we believe corporate bonds are better positioned than Treasurys—especially for our longer-maturity strategies. Accordingly, we are updating positioning in laddered-bond portfolios.

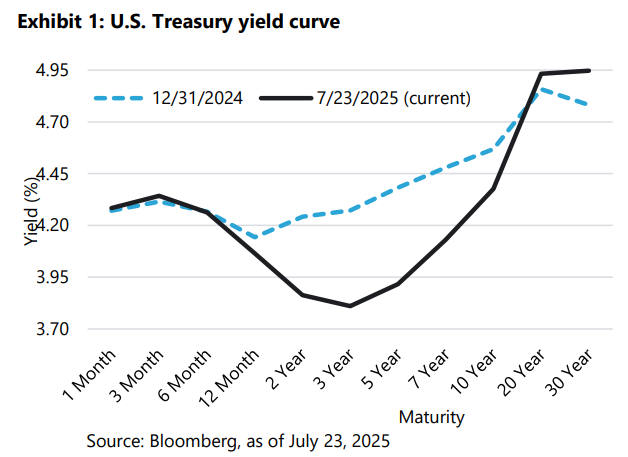

Corporates versus U.S. Treasurys

Corporate bonds are currently more attractive than comparable maturity Treasurys in a number of ways, including:

• Yield: High-quality corporate bonds offer a yield premium over Treasurys. The extra yield—or spread—acts as a cushion if rates stay elevated due to inflation risks from geopolitical instability.

• Return potential: Corporate bonds have demonstrated resilience as reflected by relatively tight credit spreads. Accordingly, if spreads tighten or remain stable, then there is an opportunity to earn extra yield.

• Risk: Corporate bonds possess credit risk and can default, while theoretically Treasurys cannot default. However, we maintain high conviction in the credit outlook for our taxable corporate issuers, as demonstrated by solid fundamentals, strong balance sheets, stable earnings, and ample cash reserves.

Fiscal uncertainty: U.S. deficit and Treasury supply concerns

A ballooning U.S. deficit—amid tax cuts and spending packages—has triggered increased Treasury issuance. This is especially true for the long end of the U.S. Treasury yield curve—putting upward pressure on yields (and downward pressure on prices). This fiscal environment makes owning long-Treasurys more unpredictable.

• The 30-year Treasury yield reached a recent peak above 5.0% in mid-July 2025, which was accompanied by outflows from long-duration Treasury funds.

• Given this, we believe the market may start to demand a higher term-premium for holding long-dated Treasurys, ultimately hurting performance for existing long-duration Treasury holdings.

• Corporate bonds are less impacted or reliant upon fiscal dynamics.

A Non-Committal Fed

Around mid-June, we saw no solid commitment that the U.S. Federal Reserve (Fed) would be lowering interest rates—supporting the view that rates may remain elevated or “higher for longer”.

• In such a climate, traditional long-Treasurys appear less attractive, while corporate bonds offer more yield cushion via credit spreads. In a prolonged high-rate environment, corporate bonds generally outperform Treasurys due to the yield differential.

• Additionally, the Fed is expected to lower the federal funds rate at some unknown date in the future, likely when inflation cools and labor indicators weaken. When the Fed decides to lower rates, our traditional strategies prefer shorter-duration U.S. Treasurys as they will move more in line with the Fed.

Macro geopolitical risk premium reassessment

Markets are dealing with considerable global uncertainty and are reassessing global risks from China, Russia, and the Middle East.

• Fixed income markets have priced in substantial fear. However, unless there is a U.S. recession—which is not our base case scenario—there should not be a further flight to quality.

• If risk has in fact normalized and the flight to quality is already priced in, then corporate bonds offer better relative value.

• Additionally, the conflict in the Middle East is expected to lead to supply-side inflation through higher energy and oil prices. Long maturity U.S. Treasurys will generally suffer more than corporate bonds due to the inflation headwind eroding returns.

Positioning changes

For new client portfolios and maturing positions for existing clients, we have updated our strategic sector position to reflect our view that corporate bonds are more attractive than Treasurys.

• For traditional Laddered Government/Corporate Bond strategies the government allocation will be reduced from 60% to 50%, while corporates will move from 40% to 50%.

• Additionally, for Traditional Intermediate and Traditional Short Term Plus strategies, we expect to favor corporate bonds over Treasurys for most longer maturities. These strategies hold bonds with maturities in the 5-to-10-year range.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice and is for educational purposes only.

Statements that are not factual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assume any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. Bonds are subject to interest rate risk and will decline in value as interest rates rise. SEI Fixed Income Portfolio Management is a team within SEI Investments Management Corporation (SIMC). Information in the U. S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).