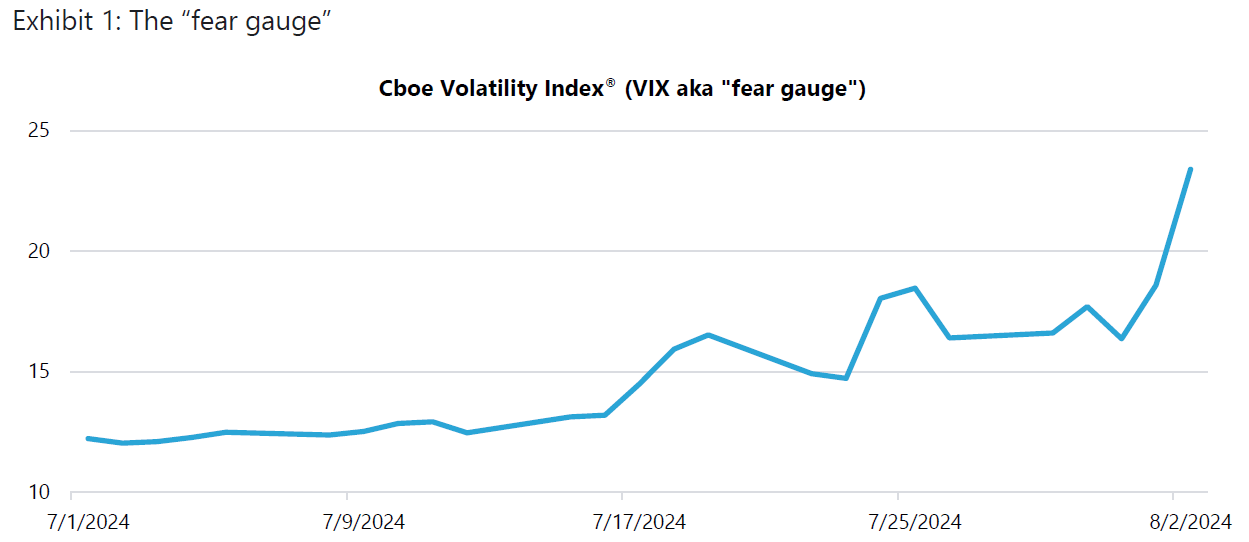

Volatility with a vengeance.

After a period of relative calm, global equity markets plunged and volatility spiked in the opening days of August. While investors are understandably concerned over the recent moves in the market, SEI manages its portfolios for the long term. We remain focused on strategic asset allocation and prudent, thoughtful portfolio management through the market’s ups and downs.

Softer economic data, accommodative central banks, and geopolitical tensions contributed to the severe and swift market moves in the opening days of August. U.S. equities fell in response to a disappointing payrolls report, and Japanese stocks soon followed suit. By the time of the opening bell in the U.S. on Monday August 5, global equity markets were in full retreat.

Our view

Markets were always going to be vulnerable to strong bouts of volatility given ongoing geopolitical tensions, a fluid political backdrop (U.S., France), the lagged effects of the interest-rates hikes the Federal Reserve (Fed) has already implemented, risk assets (equities, credit) priced for perfection, and a cooling U.S. labor market. Now, investors appear to be pricing in a U.S. recession. While we agree that the U.S. economy has hit a soft patch in the data, we do not see heightened risks of recession at this time.

Accordingly, this feels like an overreaction that is being exacerbated by the unwinding of carry trades , as well as a reevaluation of equity positions in artificial intelligence. We continue to expect that the global economy will avoid recession in the near term, and we remain focused on longer-term trends as opposed to shorter-term variations in the economic data.

Similarly, our expectations for the economy and Fed policy have not changed much. We expect the Fed will use the Jackson Hole Economic Policy Symposium later this month to “pre-announce” an interest-rate cut of 25 basis points (0.25%) in September, with one or two further rate cuts by year-end well within our expectations. With that said, the market is now pricing in a fair chance for a cut of 50 basis points (0.50%) in September, and roughly 200 basis points (2.00%) of additional easing over the next 12 months.

Our portfolios

Diversification remains our primary asset allocation objective. A short time ago, tech stocks seem to be the only thing investors cared about. Today, those once forgotten bond allocations in many diversified portfolios are serving their purpose. This is exactly why we emphasize diversification throughout the market cycle—you have to have it in place at all times if you want it be there when it matters.

Equities

While we understand the desire to take action in the face of significant market moves, we do not manage our portfolios on the basis of ever-shifting macroeconomic or geopolitical sands. This is the time to ignore the short-term noise and focus on what matters in the long term. With that in mind, we will maintain our strategic allocation to equity markets, remaining focused on quality, value, and momentum—factors that have consistently contributed to long-term portfolio returns.

We continue to expect a broader rotation in equity performance as we make our way through earnings season. We maintain our conviction in value investing and active management in general. On the latter, we continue to think that current market conditions present a prudent time to move from passive U.S. portfolios into actively managed strategies.

Fixed Income

Our fixed-income portfolios are defensive on credit and tactical in rates. We have generally been moving up in credit quality over the past 12 months, while still delivering attractive yields. We favor higher-quality holdings in the securitized market, along with corporate bonds at the front end of the yield curve. Within corporates, the financials sector has provided attractive opportunities.

In the U.S. and U.K., we are generally overweight-to-neutral rates. In our global portfolios, we are underweight duration at the aggregate level through a gloomy view on Japan, Europe, and Canada, while overweight U.S., New Zealand, Australia, and select emerging-market countries.

Longer term, wasteful fiscal spending in the U.S. remains a concern that appears unlikely to abate, regardless of the outcome in November’s election. Running large budget deficits when the unemployment rate is at historically low levels does not bode well for the debt trajectory when the next downturn does arrive. We remain convinced that investors will demand higher interest rates for longer-term debt and are positioned accordingly.

The bond market’s performance in recent weeks underscores the important role fixed income plays as a diversifier to risk assets. We noted this in October 2023, when we pointed out that the severe repricing of interest-rate risk presented investors with a more favorable yield/duration trade-off going forward—and that bonds would likely be a beneficiary of any equity market ruptures. We also highlighted that, even if inflation remained stickier for longer, fixed-income returns would be better protected thanks to a much healthier yield cushion.

Stay the course

In times such as these, it is important that investors stay the course and avoid overreacting, particularly to any single data point. For our part, we are actively managing our portfolios, seeking—as always—to adjust proactively and avoid reacting to short-term variations in data and markets.

Glossary

A carry trade involves borrowing at a low interest rate and then investing in an asset with a higher interest rate.

Credit quality refers to a security’s creditworthiness and risk of default. The higher the credit quality (or rating), the lower the perceived risk of default. The ratings for S&P Global Ratings and Fitch Ratings range from AAA (highest) to D (lowest). Moody’s Investors Service assigns credit ratings from Aaa to C. Ratings below BBB/Baa are classified as non-investment-grade, or “junk,” and are considered to be riskier.

Duration is a measure of a security’s price-sensitivity to changes in interest rates. Specifically, duration measures the potential change in value of a bond that would result from a 1% change in interest rates. The shorter the duration of a bond, the less its price will potentially change as interest rates rise or fall. Conversely, the longer the duration of a bond, the more its price will potentially change.

A factor is a quantifiable security characteristic that drives returns and can be used to explain the differences in performance between securities. Examples include value, momentum, quality, and low volatility.

Momentum is a trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

Quality comprises a long-term buy-and-hold strategy that is based on acquiring shares of companies with strong and stable profitability with high barriers of entry (factors that can prevent or impede newcomers into a market or industry sector, thereby limiting competition).

Value is a mean-reverting investment strategy that is based on acquiring assets at a discount to their fair valuations. Mean reversion is a theory that prices and returns eventually move back towards their historical average.

The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating. A steeper yield curve represents a greater difference between the yields. A flatter curve indicates that the yields are closer together.

Index definitions

The CBOE Volatility Index (VIX) measures the constant 30-day volatility of the U.S. stock market using real-time, mid-quote prices of S&P 500 Index call and put options. A call option gives the holder the right to buy a stock at a specified price; a put option gives the holder the right to sell a stock at a specified price.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There is no assurance the goals of the strategies discussed will be met. Bonds and bond funds will decrease in value as interest rates rise.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs, and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information in Canada is provided by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.