Potential benefits of adding multi-asset trend to a risk parity strategy.

Trend-based strategies offer low correlation with traditional stock and bonds investments, potential downside mitigation in protracted risk-off environments, and improved portfolio efficiency.

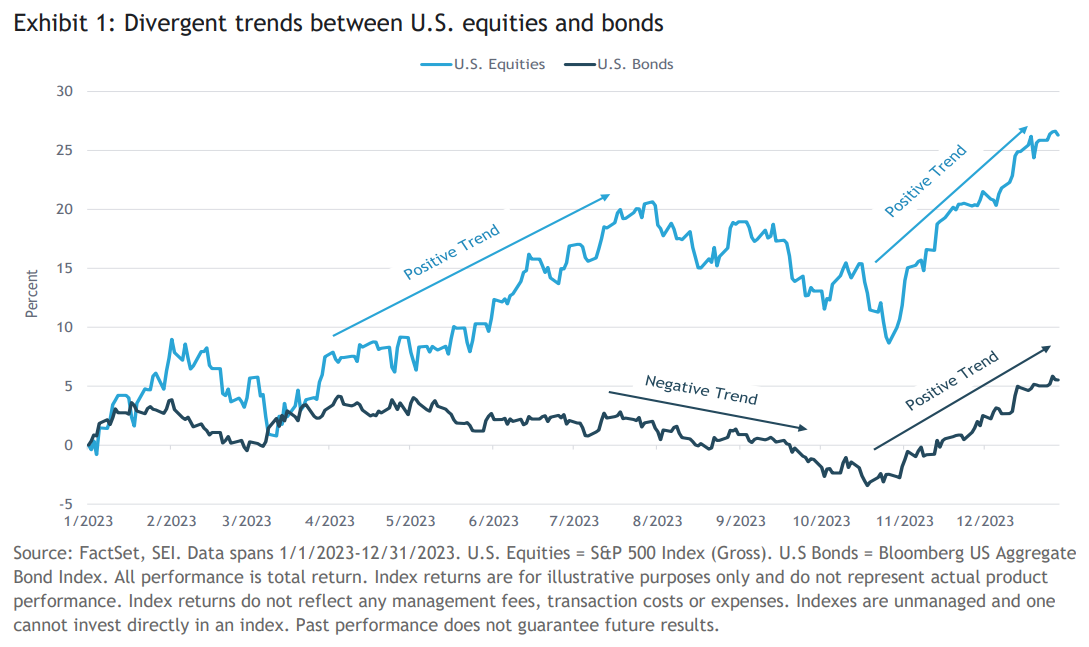

A trend-based strategy in its simplest form is one that seeks to benefit from exposure to asset types that exhibit persistent trends, both positive and negative, over time. These come in different forms, with varying speeds, but the overall concept is relatively consistent in practice. To use the U.S. equity market as an example, if the S&P 500 Index increases in value for a given time period (ex. 12 months), it has established a positive trend. Similarly, if the S&P 500 Index decreases in value for a given time period, it has established a negative trend. A trend-based strategy seeks to buy assets exhibiting positive trends, and sell assets with negative trends. Exhibit 1 below is a basic example of positive and negative trends in U.S. equities and U.S. bonds over the course of 2023.

How is trend different from momentum?

While this may sound similar to a momentum strategy, there are differences between trend and momentum. Momentum, in SEI’s implementation, is a long-only and equity-only approach, while trend is a multi-asset strategy that can go long and short, both within and across asset classes. In practice, this means that a momentum strategy would emphasize stocks with relatively good momentum, even when they are delivering negative absolute returns, whereas a trend strategy would have the flexibility to sell them short. Despite their similarities, trend and momentum are distinct investment strategies.

Why does trend exist?

Much of the theory behind the persistence of trend is rooted in behavioral finance, specifically the behavioral biases of anchoring and adjustment. These biases occur when investors underappreciate meaningful new developments, leading to share prices that do not fully reflect all relevant information. As new information or asset prices move from the investor’s anchor level, they must continually adjust their expectations. This can also be explained by the concept of fear of missing out, where investors chase stocks at higher prices to avoid missing out on projected future gains. Others have suggested that trend premiums are a reward for bearing additional risks, such as risks associated with sudden changes in market direction, or short-term underperformance. While these risks are real, diversifying trend exposures across different asset classes can mitigate them for the most part.

Why use a trend-based strategy?

Trend-based strategies can complement multi-asset strategies, such as risk parity. Risk-parity investment strategies have allocations designed to seek equal contributions to risk from their various underlying asset classes. Over time, trend-based strategies, such as those that take long positions when an asset is above its 200-day moving average and short positions when it is below, have provided a positive return or premium while exhibiting low levels of volatility and relatively low correlations to traditional asset classes. For instance, studies using proxies such as the S&P 500 Index for equities, the Bloomberg US Aggregate Bond Index for bonds, and the Bloomberg Commodity Index for commodities have shown that from 1980 to 2020, trend-following strategies applied across equities, commodities, currencies, and bonds exhibited an annualized Sharpe ratio increase of 44-52% compared to traditional strategies1. Trend strategies that take long and short positions also offer the potential for positive returns in both up and down markets. In fact, historical data suggests that trend strategies tend to perform best at market extremes— positive or negative—the very time periods where traditional asset classes tend to offer the least diversification2.

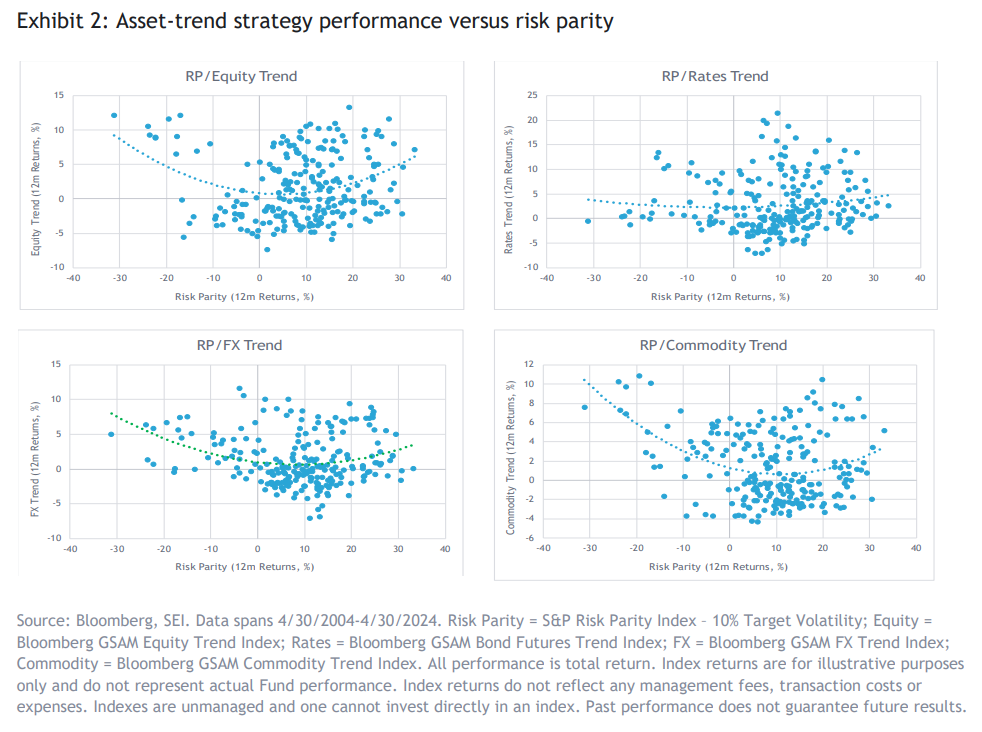

Exhibit 2 compares the performance of the S&P Risk Parity Index against various trend strategies, including equities, bonds, commodities, and currencies. The performance of the risk-parity index is plotted on the horizontal axis, while trend strategies are plotted vertically. The dots represent the returns of a given trend strategy at various levels of risk-parity performance. The blue dotted line approximates the pattern of performance for a trend strategy during the measurement period. The charts show trend performing well at both positive and negative extremes for risk parity, while providing modestly positive performance in more muted periods, on average.

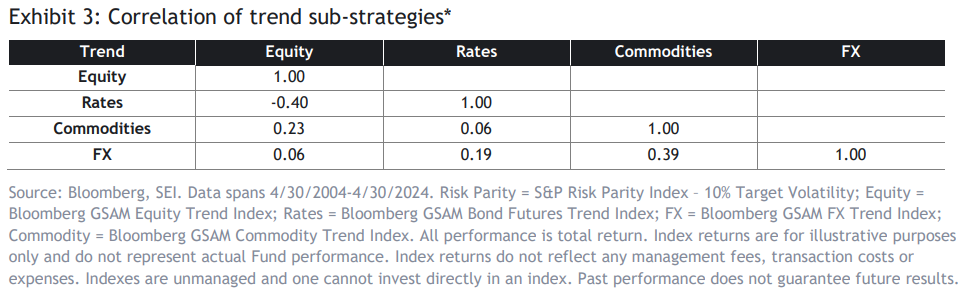

Not only do trend strategies have the potential to provide meaningful diversification benefits to the traditional asset classes held in risk-parity strategies, underlying trend strategies confer these benefits on one another as well. The correlation matrix in Exhibit 3 measures the correlation of individual trend strategies over a 20-year period. Correlations range from -0.40 to 0.39, with an overall average correlation of 0.09 between the pairs of asset types. Our preference for multi-asset trend strategies is rooted in this low correlation. We believe that in the context of a broader portfolio, this implementation has the potential to enhance investment outcomes over time.

Bringing it all together

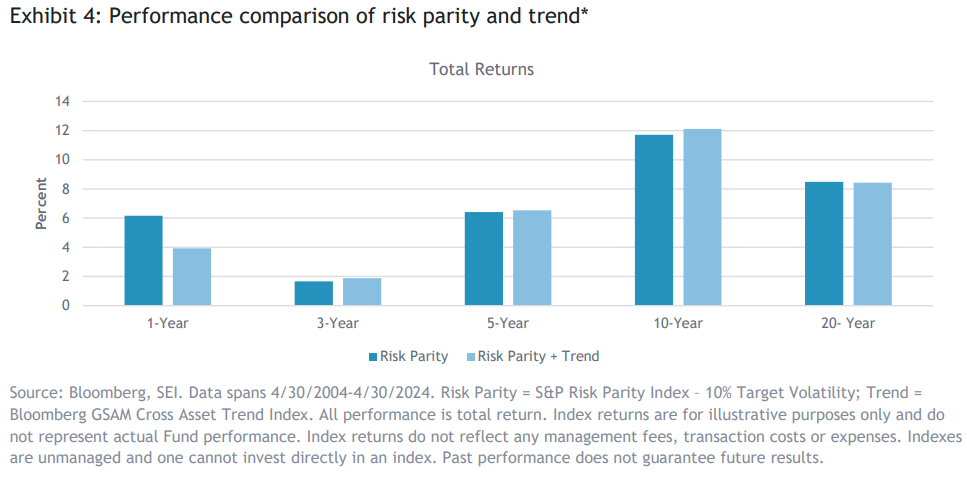

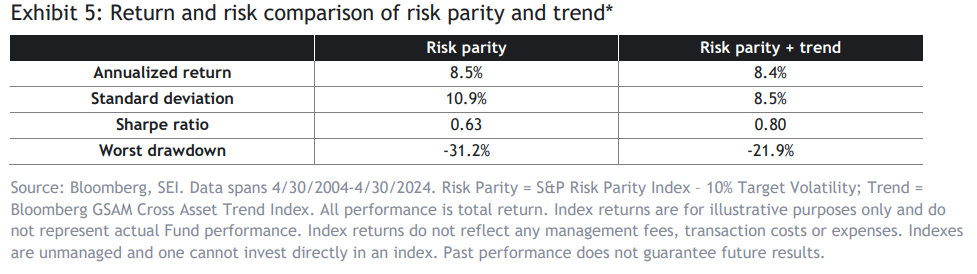

We believe that adding a cross-asset trend strategy, even a relatively modest allocation, can benefit a risk-parity portfolio. For illustrative purposes, we have analyzed the historical benefit of adding cross-asset trend to a risk-parity strategy at a 20% risk weight. We consider this risk allocation to be near the high end of a range for most investors. Exhibits 4 and 5 compare the S&P Risk Parity Index to a blended portfolio, with 80% of the risk weight allocated to the S&P Risk Parity Index and the remaining 20% allocated to the Bloomberg GSAM Cross Asset Trend Index (which allocates to the four aforementioned individual asset classes).

Over the full measurement period, the blend of risk parity and trend produced a similar annualized return to the risk-parity index, albeit with less volatility, resulting in a higher Sharpe ratio. Furthermore, the addition of trend meaningfully reduced the worst drawdown or peak-to-trough decline. In periods of stress for traditional asset classes, trend strategies have been able to provide an additional level of diversification. This is particularly important, as correlations of traditional asset classes tend to increase in significant down markets. 2022 represents a recent example where an allocation to trend could have improved investment outcomes. As soaring inflation and higher interest rates negatively affected both stocks and bonds, trend strategies were among the few strategies that delivered positive performance. That noted, trend strategies also have their weaknesses; they can be susceptible to short-lived market environments, such as market reversals, that lack trend features. Longer term, our research has found that the impact of an allocation to trend has been positive.

Benefits of multi-asset trend

The integration of a multi-asset trend strategy into a risk-parity portfolio represents a strategic move towards enhancing portfolio performance and risk management. The historical resilience of trend strategies, particularly during market extremes, underscores their potential to provide meaningful diversification benefits. Trend strategies’ low correlation with traditional asset classes, and among themselves, further bolsters the case for their inclusion in a multi-asset portfolio. While the core of an investor’s portfolio should continue to emphasize time-tested investments such as equity, credit, and term, the addition of a diversified trend strategy can serve as a valuable counterbalance, particularly during periods of heightened market volatility and increased correlation among traditional asset classes. As we navigate the complexities of today’s financial markets, the ability to adapt and innovate remains paramount.

*Exhibits 2 through 5 contain performance prior to the indices’ inception date, which is back-tested. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns. Past performance is no guarantee of future results.

Important information

Information in the U.S. provided by SEI Investments Management Corporation, a federally registered investment advisor and wholly owned subsidiary of SEI Investments Company (SEI).

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice. This information is for educational purposes only. Certain information contained herein has been provided to SEI by an unaffiliated third party. SEI cannot guarantee the accuracy or completeness of the information and assumes no responsibility or liability for its incompleteness or inaccuracy.

There are risks involved with investing including loss of principal. There is no assurance that the objectives of any strategy will be achieved or will be successful. No investment strategy, including diversification, can protect against market risk or loss.