Healthcare productivity growth—a second opinion?

Productivity growth is the holy grail of macroeconomics. All else equal, it supports higher standards of living and lower inflation.

But how do we measure it?

Art Patten, CFA Client Portfolio Strategist Observing changes in productivity on a factory floor is far easier than gauging services-based businesses and industries. The issue is amplified when aggregating regionally, nationally, or globally—modern economies include a wide range of businesses, many of which transact in services rather than tangible goods.

As a result, productivity-growth estimates are subject to meaningful measurement bias and should be interpreted with caution. Nevertheless, productivity growth is important enough that economists and statistical agencies must attempt to measure it.

If those estimates capture directional trends, they’re useful. Even if the numbers aren’t perfect, they influence how we think about labor allocation, inflation pressure, living standards, and the economic burden of healthcare.

Why healthcare productivity measurement matters

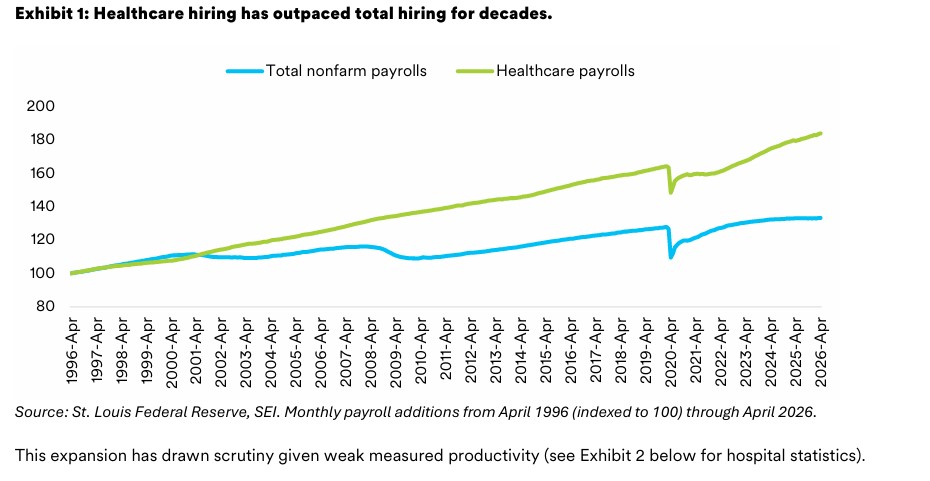

These concerns are especially timely and relevant to healthcare, where employment has continued to grow in recent years, reflecting, in part, aging populations. The growth in healthcare employment in the U.S. is highlighted in Exhibit 1.

That makes measurement more than an academic exercise, as rising employment in an economic sector with low or negative productivity growth implies downward pressure on living standards and upward pressure on inflation. In short, if healthcare is absorbing a growing share of labor, the difference between weak productivity and poorly measured productivity has real macroeconomic implications.

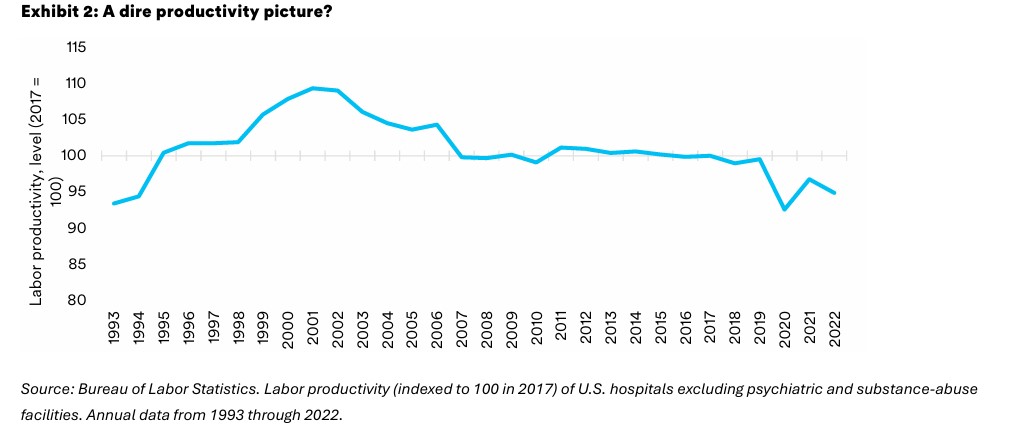

Healthcare productivity growth is especially difficult to measure and has historically appeared slow—sometimes even negative, as Exhibit 2 indicates. Some industry observers take those estimates at face value; others contend healthcare requires a nuanced, technical approach.

As a research piece from Brookings acknowledged in 2009,1 most studies had shown poor productivity dynamics in medical care across countries; however, the author cautioned that these findings were “highly suspect,” given the degree of innovation in healthcare and the sector’s well-documented productivity-measurement challenges.

What the BEA study found

In March, the U.S. Bureau of Economic Analysis (BEA)2 tried to get a firmer handle on those dynamics. The study’s methods reveal how challenging it is to measure productivity accurately in certain medical industries. While numerous economists have made similar attempts, the BEA advanced the literature by integrating innovative measurement techniques from prior studies. Inputs were estimated costs of the services delivered, while outputs were health outcomes for nine specific health conditions.

The results were both surprising, given longstanding estimates of weak productivity dynamics, and encouraging, implying healthcare productivity growth may be stronger than traditional estimates project. For an industry expected to continue hiring at a solid pace in a world of aging populations and stubborn inflation, that’s reassuring news. It may also be constructive for healthcare occupations, as stronger productivity growth can support higher labor compensation costs over time.

Of course, as with any economic research—especially into productivity growth—there are important caveats. The study focused on a small number of specific health conditions rather than the general practice of medicine and supporting industries, and its findings will need to be evaluated through further research and across other geographies.

Still, the takeaway is important: Healthcare productivity growth has likely been understated for decades. Medical care has long operated under constraints—public- and private-sector reimbursement practices, layers of government regulation, volatile subsidies for underserved geographies and populations, burdensome capital budgets, tight operating margins, and persistent labor pressures to name a few—so it’s welcome news that productivity dynamics might be better than previously thought.

From an economic perspective, these findings should also ease concerns that continued hiring in healthcare will weigh on overall productivity or add meaningfully to inflation pressure. Inflation is likely to remain stubborn in the years ahead, but healthcare may not be the productivity sinkhole traditional estimates imply.

We can’t measure healthcare productivity perfectly, but better measurements suggest it may not be as weak as previously reported. Advances in artificial intelligence may offer an incremental tailwind to productivity over time, though the extent and measurability remain uncertain. For a sector expected to keep hiring as populations age, that’s a meaningful second opinion.

GLOSSARY AND INDEX DEFINITIONS

For financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

IMPORTANT INFORMATION

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice).

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assume any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only. Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).