Capital market assumptions update.

SEI’s Advice and Asset Allocation Group updated our capital market assumptions (CMAs). Fixed-income assumptions were reworked to reflect possible future rate paths. Equity return assumptions edged higher given higher short-term risk-free rates.

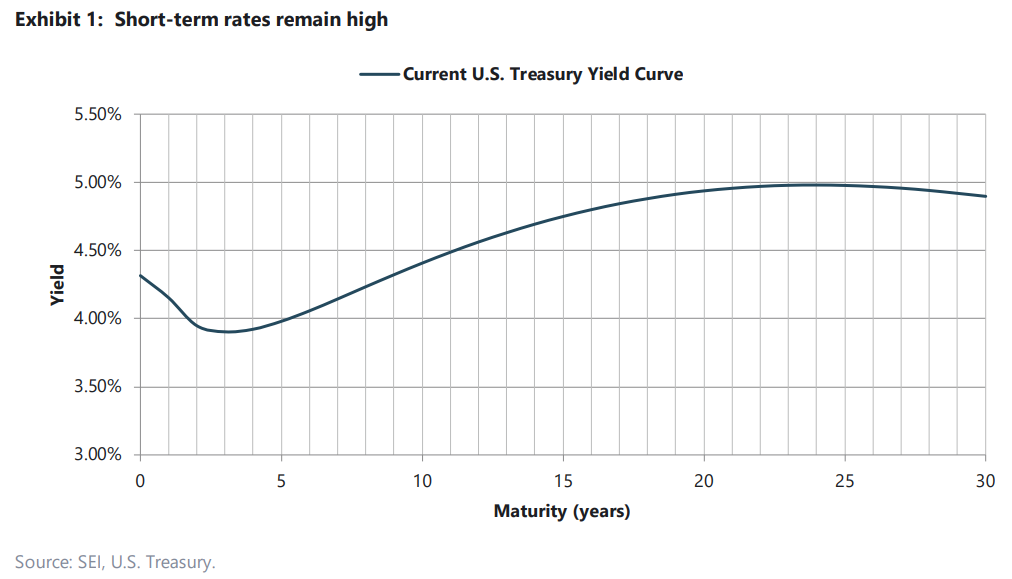

Fixed-income revisions: Inflation is the primary concern The U.S. Treasury yield curve is still inverted as of this writing, and there is a lot of uncertainty surrounding the path of interest rates and inflation. While our long-term expectations still reflect a return to a normal-shaped yield curve, the exact timing and path remain unclear. Our cash-return assumption has slightly increased from last year, but this only reflects the fact that short rates remain higher than long-term expectations. We still expect a steepening in the curve, with short rates coming down.

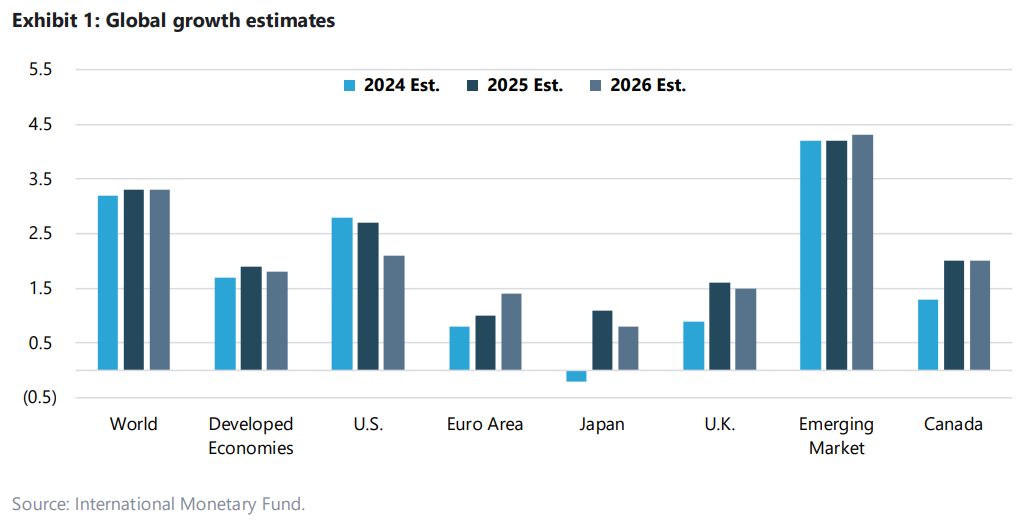

Global equity return expectations revised slightly higher

Our equity assumptions reflect higher interest rates on so-called risk-free government bonds, which serve as a core component of discount rates applied to asset classes across all risk markets. We have not changed our outlook for equity risk premiums over the span of an entire market cycle. Given this interaction, we expect equity returns to be higher over the long run than projected in the recent past.

Process overview

CMAs are an integral part of our strategic asset allocation process. Each reevaluation is led by forward-thinking, qualitative judgments that are guided by empirical data.

Estimating CMAs requires extensive analysis of the key drivers of risk and return in each asset category. These assumptions are not economic predictions of how asset classes will perform over a given period; instead, they are baseline estimates of long-term asset-class characteristics. CMAs are used to form our strategic asset allocation portfolios.

We maintain a CMA model that contains risk, return, and correlation assumptions across global asset classes and currencies. A combination of quantitative analysis of historical data and qualitative judgment is used to capture trends, structural changes, and potential scenarios not reflected in historical data.

Our process is represented as follows:

We estimate asset-class returns by focusing on the average risk-adjusted return (Sharpe ratio) that we feel an asset class is expected to deliver over full market cycles

• Equity return assumptions are built by applying our assumption of risk to the asset class Sharpe ratio determined above and adding this to the short-term risk-free rate.

• Fixed-income return assumptions reflect both long-run equilibrium conditions and the current yield environment. Equilibrium return estimates account for the short-term risk-free rate, maturity premium (typical upward slope of the government yield curve), credit spreads, and expected losses due to defaults and downgrades.

• Our model includes assumptions for currencies, allowing CMAs to be translated from local-currency terms to different currency perspectives.

• Asset-class risk assumptions account for tail risks directly by assessing potential extreme market scenarios. Standard deviation estimates are derived to be consistent with those tail risks.

Asset-class risks and correlations

Risk and correlation assumptions can use history to a larger degree than return assumptions. However, risks and correlations do change as economic fundamentals change; therefore, it is important to focus on the most relevant periods of history and make qualitative adjustments where appropriate.

Further insights into our risk and correlation assumptions are as follows:

• Risk: Investor perceptions of risk are generally most concerned with the left tail of return distributions. Accordingly, asset-class risk assumptions are meant to capture the frequency and severity of negative returns. We estimate tail risks directly by assessing the potential extreme market scenarios that could occur and then derive the standard deviation that’s consistent with those tail risks.

Correlation: During an economic downturn, correlations among risky assets tend to rise, while correlations between safe haven assets and risky assets tend to fall. We consider several different scenarios for correlations, including a baseline scenario as well as stress scenarios in which correlations are typically assumed to be higher than the baseline. Under our stress scenarios, we raise correlations halfway between their baseline levels and 1.00 (perfect positive correlation). We generally seek to set baseline correlations high enough that the corresponding stress correlations approach the highest historical correlations over rolling periods. This method seeks to ensure that assets that tend to experience sharp losses at the same time are not unduly rewarded for their illusory diversification advantages.

Summary

The result of our analysis is a series of inputs that produces a picture of how we believe portfolios are likely to behave, on average, through time. The true value of the analysis is in understanding the relationships between asset classes rather than accurately predicting performance over finite periods of time. Our CMAs are intended to reflect the behavior of asset classes over several market cycles. Stress assumptions are also examined, since the characteristics of asset classes are constantly changing. A dynamic model is employed to manage the numerous assumptions required to estimate portfolio characteristics under different base currencies, time horizons, and inflation expectations.

About SEI’s capital market assumptions

SEI Investment Management Corporation (SIMC) develops forward-looking, long-term capital market assumptions for risk, return, and correlations for a variety of global asset classes, interest rates, and inflation. These assumptions are based on historical analysis, current market environment assessment, and qualitative reasoning. We believe this approach is more impartial than using pure historical data, which is often biased by a particular period or event.

The asset-class assumptions are aggregated into a diversified portfolio so that each portfolio can then be simulated through time using a Monte-Carlo simulation. This approach enables us to develop scenarios across a wide variety of market environments so that we can educate our clients about the potential impact of future market variability over time. We believe our approach enables our clients to make more informed decisions related to the selection of their investment strategies.

For more information on how SIMC develops capital market assumptions, please refer to the SEI paper, “Executive Summary: Developing Capital Market Assumptions for Asset Allocation Modelling.” Further information on the actual assumptions used may be requested from your SEI representative.

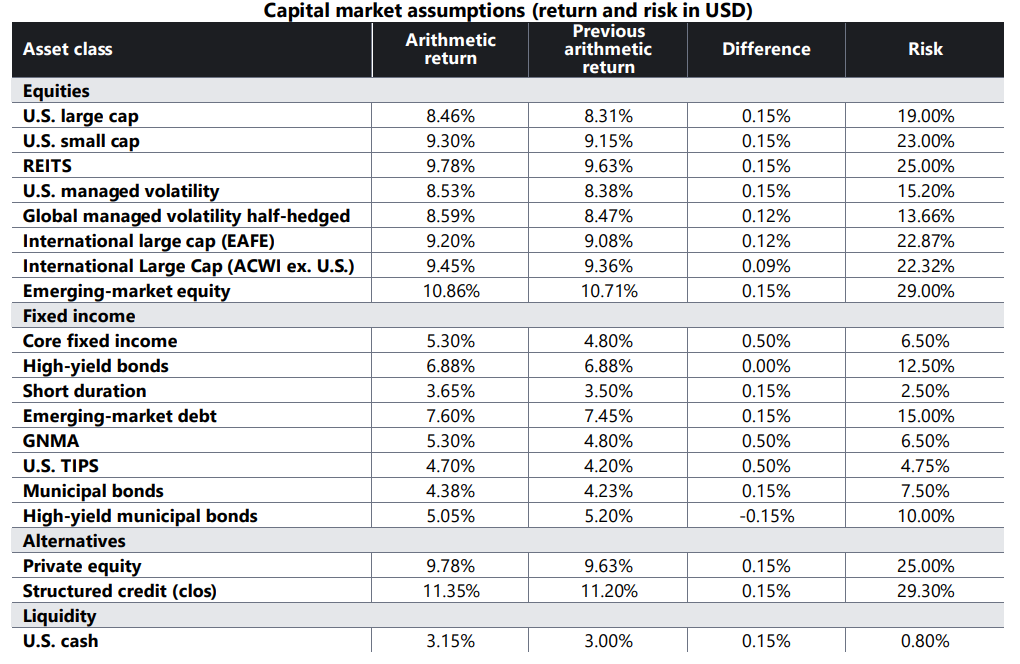

CMAs are not predictions of how asset classes will perform or reliable indicators of future performance; instead, they are expected long-term characteristics of asset classes. The below figures are SEI’s mean estimates for select asset classes. They do not represent all asset classes SEI evaluates nor should they be considered projections for any SEI investment products. Different tools and models can simulate various market conditions using these assumptions as inputs. CMAs are used in the strategic asset allocation process, for asset/liability studies, and in proposal-generation systems. All assumptions are pre-tax and gross of any fees or expenses related to investing.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is for educational purposes and should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds. There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There are other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. Past performance does not guarantee future results. Index returns are for illustrative purposes only and do not represent actual portfolio performance. Index returns do not reflect any management fees, transaction costs or expenses. One cannot invest directly in an index.

Information provided by SEI Investments Management Corporation, a wholly owned subsidiary of SEI Investments Company (SEI). Information contained herein that is based on external sources is believed to be reliable, but is not guaranteed by SEI, may be incomplete or may change without notice.